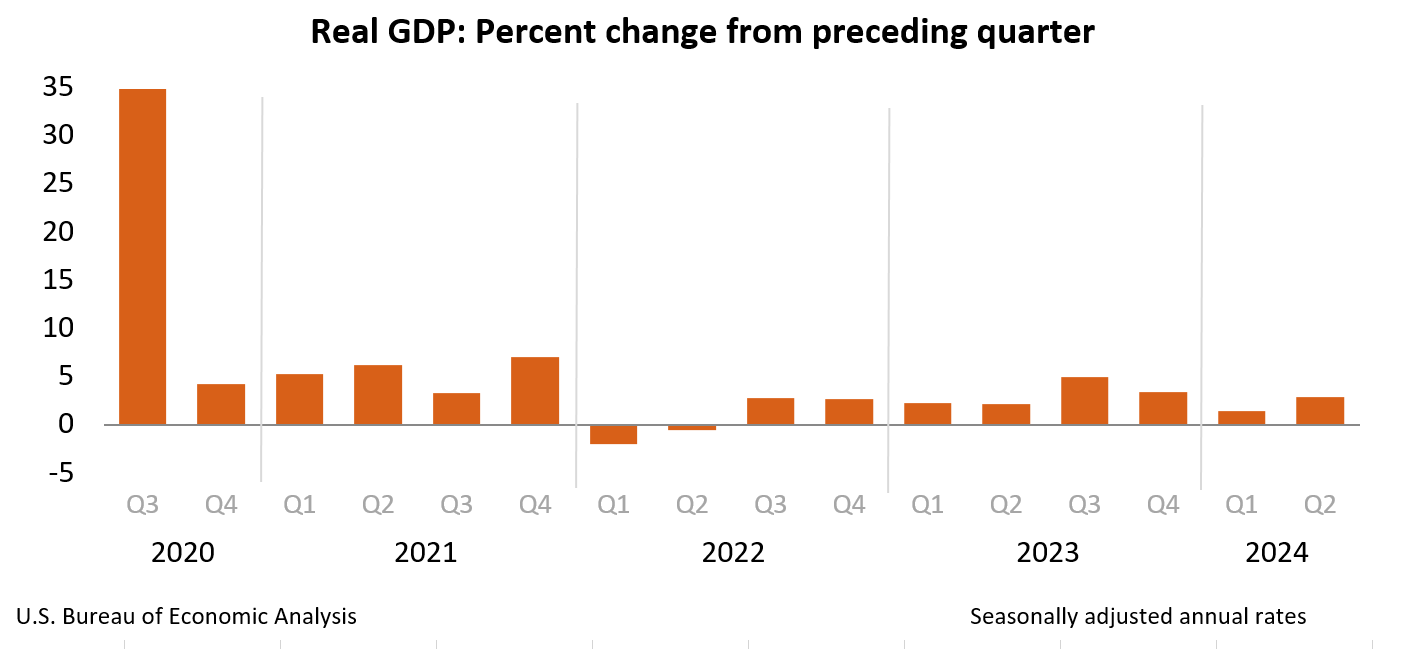

According to the Bureau of Economic Analysis, the US economy expanded at an annualized rate of 2.8% in the second quarter, up from 1.4% in the first quarter and above the consensus forecasts of 2%.

Consumer spending accelerated from the first quarter, climbing from a 1.5% annualized rate to 2.3%. Goods consumption spurred the rebound, which rose at a rate of 2.5% in Q2 after falling at an annualized rate of -2.3% in the first quarter. Motor vehicles, recreational goods and vehicles, and gasoline led growth in goods consumption while services slowed from a rate of 3.3% last quarter of 2.2%.

Notably, private inventories contributed positively to consumption during the quarter after being a drag on it during the last two quarters.

Residential investment contracted for the first time in a year while non-residential investment accelerated from a 4.4% rate to 5.2%, led by equipment, which grew at more than eight times the rate in the first quarter.

Government spending accelerated in Q2, led by defense, while net trade continues to drag down growth as imports rose faster than exports.

2. BEIGE BOOK

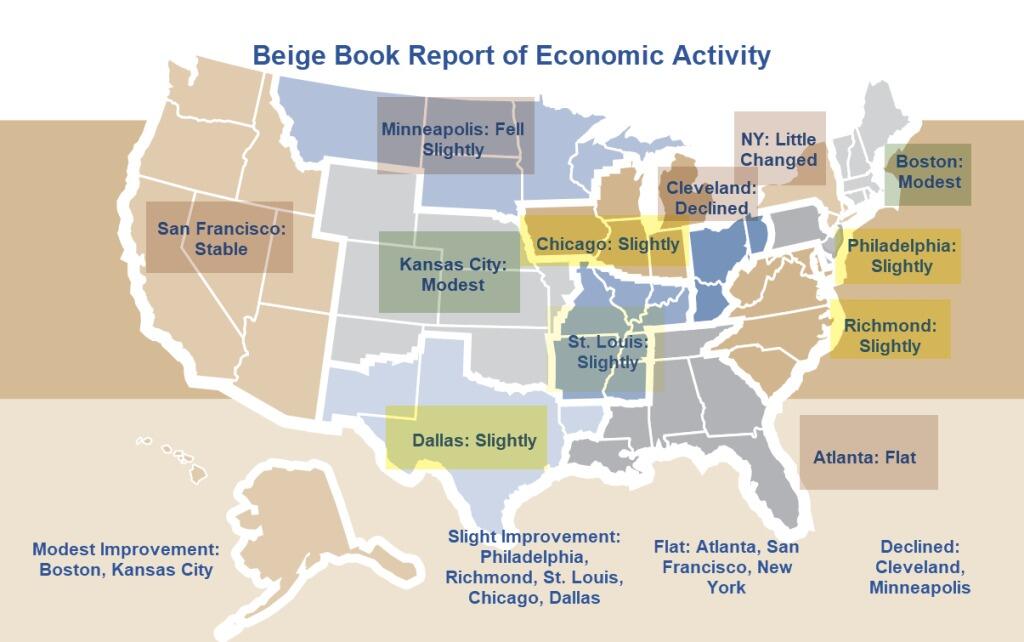

The Federal Reserve’s Beige Book summary of economic activity reported that in the six weeks ending on July 17th, the US economy grew at a slight to modest pace in most districts, but five of the twelve districts reported flat or declining activity.

The data reflects activity that is also captured in this week’s second-quarter GDP estimate but offers an under-the-hood snapshot of the US economy’s regional differences, labor market activity, and economic sentiment.

While the advanced estimate of second-quarter GDP released on Thursday reported an acceleration from the previous quarter, the five districts reporting flat or declining activity in the most recent Beige Book also accelerated— three more than the last report.

Wages continue to grow at a modest to moderate pace in most districts, the Fed reports. Prices also rose modestly, while household spending was little changed. The interactions of these three metric trends over the next several weeks will play a critical role in determining whether policymakers move forward with a widely expected September interest rate cut.

Many districts noted softer demand for consumer and business loans while reported activity on residential and commercial real estate markets varied. Travel and tourism were roughly on par with seasonal expectations, and a retail inventory buildup spurred notable growth in the transportation sector.

Expectations for the six months ahead forecasted slower economic growth stemming from uncertainty around the US election, domestic policy, geopolitical conflict, and inflation.

3. INTEREST RATE FORECAST

The stronger than expected second quarter GDP report shifted market expectations for number of rate cuts that will take place in 2024, though expectations for the timing of the first rate cut have largely held.

According to the Chicago Mercantile Exchanges Fed Watch Tool, there is still an 88.2% chance of a September rate cut, down from 92.0% one week ago.

On the day before the Q2 GDP report, futures markets projected a 52.7% change that there would by three quarter-percentage point rate cuts by the end of year. However, by the end of the trading day on Thursday, an overwhelming 87.7% forecast the policymakers will hold rates steady through the end of the year following an initial cut in September.

4. MID-YEAR COMMERCIAL PROPERTY OUTLOOK

A recent mid-year report from Capital Economics forecasts that transaction activity is likely to bottom out over the summer months — but that valuations may have more declines to undergo before similarly inflecting.

The report’s analyst suggests that valuations would need to fall an additional 12% from Q1 levels to properly reflect the impact of higher interest rates. This will show up through rising cap rates, which they expect to climb another 80 bps before reaching a cyclical peak at the start of next year.

Treasury yields are forecasted to stay elevated this year despite the prospect of rate cuts, while the report projects NOI yields to climb further in 2025 as the market rebuilds yield gaps to adjust to the new rate path before stabilizing in 2026.

Office yields are expected to see the largest rises to close 2024, while industrial and apartments are expected to lead the way after, though the latter two sectors are projected to be first and second in rent growth between 2024-2028, respectively.

5. REIT MID-YEAR REPORT

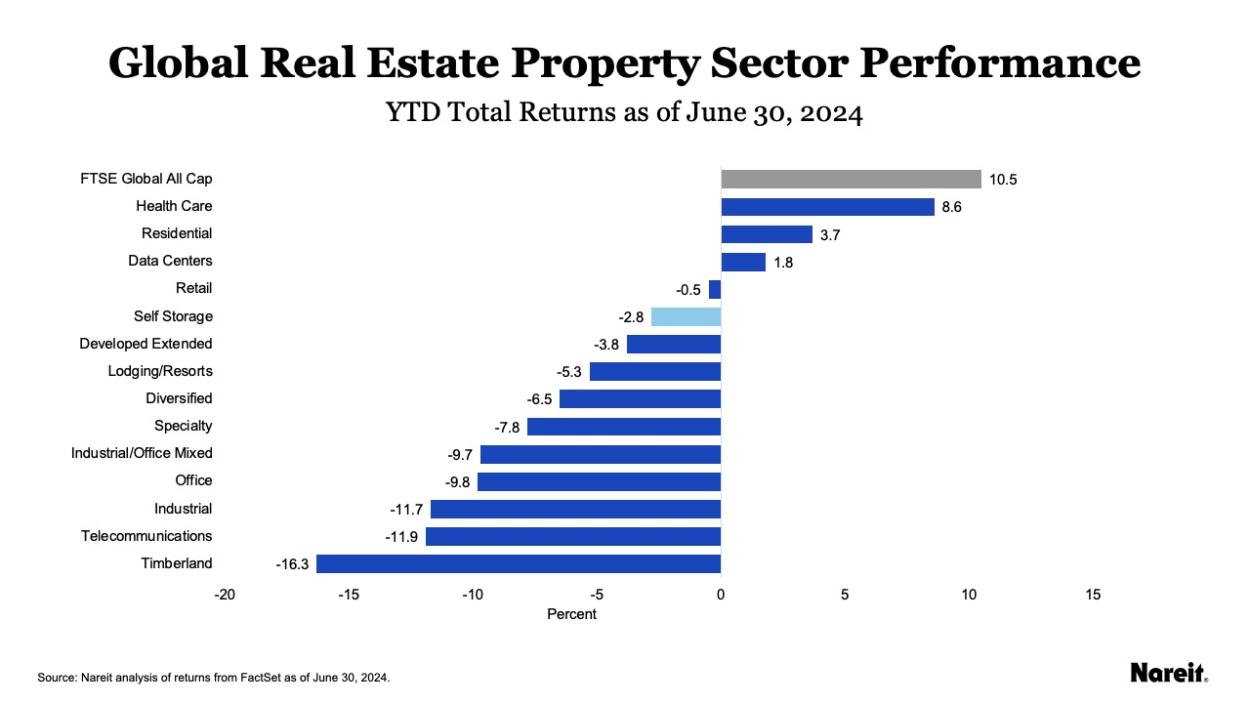

Nareit reports that through June 30th, the FTS EPRA Nareit Developed Extended Index, an index series made up of REITs and global publicly listed real estate assets, was down 3.8% on a year-to-date basis.

While in contraction, the latest data is an improvement from a 9.4% decline in mid-April that coincided with a spike in Treasury yields.

Health care (+8.6% YTD), residential (+3.7% TYD), and data center (1.8% YTD) REITs have outperformed others in 2024. Timber (-16.3% YTD), telecommunications (-11.9% YTD), and industrial (-11.7% YTD) REITs, which represent close to a third of the index, have lead declines.

6. CONFERENCE BOARD US ECONOMIC FORECAST

According to the Conference Board’s recent forecast for the US economy, released two weeks before the second-quarter GDP advanced estimate, GDP growth is expected to continue to slow in 2024 before picking up at year’s end and into 2025.

The report forecasts a slowing economy in the short term as elevated prices and interest rates continue to sap demand. The forecast relied on first-quarter data that showed a dramatic deceleration in US GDP growth to just a 1.4% annual rate, down from 3.4% in the fourth quarter of 2023. Second-quarter 2024 GDP estimates were not yet available, but growth rates of 2% and 1% in the second and third quarters, respectively, were assumed in these projections.

An acceleration of GDP growth at the turn of the year and into the next as inflation subsides and the Fed begins rate cuts. However, the trend of inflation in the next couple of months and the timing of the Fed’s first rate cut will dictate when this potential acceleration would begin.

7. CHIP AND SCIENCE ACTS SPUR CRE DEMAND

A recent GlobeSt article investigates the impact of the CHIPS and Science Acts on commercial estate markets, as the 2022 laws introduced $52.7 in new spending, including both funding and incentives, for R&D and manufacturing in key science and tech sectors.

The Texas market of Sherman-Denison was a key recipient of new federal funds with new semiconductor plants built by players like Texas Instruments and GlobiTech. The medium-term impact on the market includes the addition of up to 5,000 new jobs, bringing new residents and housing needs. The region is currently home to just 6,800 apartment units, reflecting the need for developers to fill the impending shortage.

While the Real Page data underpinning the Sherman-Denison example focused on the multifamily impact, the article notes that retail demand has also likely increased, with school and healthcare needs likely to follow.

Economists largely expect the laws to incentivize companies to increase manufacturing in the US and will benefit regions with strong labor force dynamics, available skills, and a diverse supplier base—thereby increasing demand in local real estate sectors. However, whether the economic stimulus of the medium-term investment in these sectors is sustained remains to be tested and will help determine the long-term viability of such CRE investments.

8. NAHB HOUSING MARKET INDEX

According to the latest NAHB Housing Market Index (HMI), builder confidence in the market for single-family homes fell by one index point in July from the previous month.

The downtick is a declaration from May and June, which saw the index decline three and two index points month-over-month, respectively.

Present sales conditions fell during the month while expected sales conditions in the next six months rose, and traffic of prospective buyers declined.

The July survey also showed that builders are increasingly cutting prices to bolster home sales, with 31% of all builders doing so in July compared to 29% in June and 25% in May.

Despite the increased price cutting, the report notes that the average home price reduction held steady at 6% for the 13th straight month.

9. EXISTING HOME SALES

According to the latest data from the National Association of Realtors, existing home sales declined by 5.4% between May and June to a seasonally adjusted annualized rate of 3.89 million units, the sharpest decline since 2022.

June saw the fewest number of sales so far this year, and it was the fourth consecutive monthly decline in existing home sales, with median home sales prices climbing to a record high of $426,900.

Unsold housing inventory rose by 3.1% from May to 1.32 million units, the equivalent of 4.1 months of supply at current housing prices.

10. RETAIL SALES

US retail sales stalled in June, according to the latest data from the US Census Bureau.

Following an upwardly revised 0.3% increase in May, retail sales were flat month-over-month. Sales at gas stations were down 3.0%, and sales for autos dropped 2.3%. Sales also fell at sporting goods, hobby, music, and bookstores.

Meanwhile, sales at non-store retailers rose during the month, climbing 1.9% from May. Building materials and garden equipment sales were up 1.4%, while sales at health and personal stores rose 0.9%. Other items such as clothing, furniture, electronics and appliances, general merchandise, and food and drinking places also increased sales during the month.

All in all, excluding gasoline, retail sales were up 0.2% in June, suggesting that consumer cutbacks in gas demand are not translating into a decline in broader consumption.