US Consumer Confidence dipped sharply in March, according to the Conference Board’s latest numbers.

The index fell 7.2 points to 92.9, its fourth consecutive monthly decline and lowest reading since January 2021. The reading fell short of expectations.

Consumers’ increasing concerns about their financial futures are weighing down on the index as the measure of Americans’ short-term expectations for income, and the job market is now at its lowest level in 12 years.

The present-situation part of the index remains higher but is also on a downtrend as consumers signal increasing anxiety over tariffs and inflation.

The Conference Board notes that the metric of short-term expectations is well below the recession-indicating threshold of 80. Meanwhile, the share of US consumers anticipating a recession sits at a nine-month high.

2. BUSINESS UNCERTAINTY

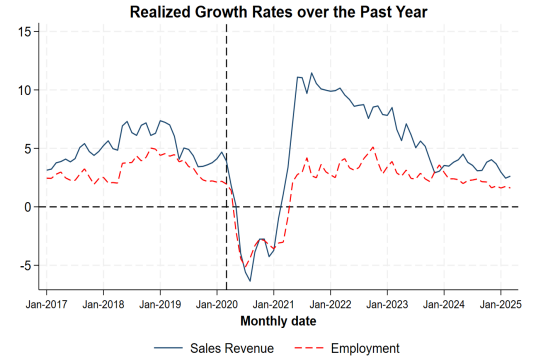

The Atlanta Federal Reserve’s latest monthly survey of business uncertainty shows that sales revenue growth expectations have risen recently, but firms remain more uncertain about future sales growth than they were prior to the pandemic.

The panel of senior finance and managerial professionals has reported considerably slower nominal sales growth over the past two years. The past several months have seen a modest revival of sales growth expectations. However, elevated uncertainty leaves current forecasts on a shakier footing than estimates made under less volatile economic conditions.

Expectations around year-ahead employment growth have similarly improved, while uncertainty about unemployment growth has returned to pre-pandemic levels. As of March, most firms don’t foresee drastic changes to working arrangements over the coming year, with fully in-person employees accounting for 68.1% of full-time workers.

3. FED INTEREST RATE DECISION

Fed policymakers kept interest rates unchanged at their March meeting, holding the federal funds rate at 4.25-4.50%, which was in line with market expectations.

In its post-meeting statement, the FOMC acknowledged that the uncertainty around the economic outlook had increased and that they were attentive to risks on both sides of its dual mandate.

Despite the nod to rising uncertainty, officials affirmed their expectations of reducing rates by an additional 50 basis points (bps) by the end of the year, which, for context, is in line with their December 2024 projection.

The Fed statement highlights that recent indicators show continued economic expansion with a stable unemployment rate and solid labor market conditions. They also noted that inflation remains somewhat elevated and that they will continue to monitor incoming data and its potential implications on the economic outlook.

4. FOMC ECONOMIC PROJECTIONS

The FOMC’s latest Summary of Economic Projections, released during every other policy meeting, cut the median GDP growth forecast for 2025, 2026, and 2027 compared to December while raising forecasts for PCE inflation in 2025 and 2026.

The median real GDP growth forecast for 2025 was cut from 2.1% in the December projections to 1.7% as of the March projections. The real GDP forecast for 2026 was revised down from 2.0% to 1.8%, and 2027 revised from 1.9% to 1.8%.

The median PCE inflation forecast for 2025 was raised from 2.5% to 2.7%. For 2026, the inflation forecast is up slightly from 2.1% to 2.2%. The Committee kept the inflation forecast for 2027 unchanged at 2%.

The unemployment rate is expected to be slightly higher this year at 4.4% compared to 4.3%, but no changes were made for the 2026 and 2027 forecasts, each at 4.3%.

5. NAIOP INDUSTRIAL SPACE DEMAND FORECAST

According to NAIOP’s Q1 2025 Industrial Space Demand Report, in 2024, the Industrial sector experienced its lowest annual rate of net absorption in 13 years.

NAIOP reports that Industrial net absorption in the second half of 2024 totaled 96.9 million square feet, bringing the annual volume to just 170.8, its lowest since 2011.

The report notes that elevated long-term interest rates have been a key reason for slowing space demand.

Analysts forecast that net absorption will slow further during the first half of 2025 to a projected 52.2 million square feet before accelerating in the second half to end the year with a total of 156.4 million square feet absorbed.

In 2026, Industrial net absorption is expected to climb back to 224.9 million square feet as elevated interest rates are expected to gradually normalize, though not return to the low-rate equilibrium of the past decade.

6. FASTEST GROWING CITIES

According to a Business Insider analysis of the recently released 2024 metro-level population estimates by the US Census Bureau, most US metros saw populations increase last year, while Florida metros were among the fastest.

Ocala, Florida (FL) and Panama City, FL, grew by 4.0% and 3.8%, respectively, last year. Meanwhile, Myrtle Beach, South Carolina, aligned with Panama City’s 3.8% growth.

Another notable Florida metro includes Lakeland-Winter Haven, which grew by 3.5%. Provo, Utah, and Daphne, Alabama, were honorable mentions at 3.0% each.

Immigration was key to the growth, with each metro area experiencing positive net international migration during the year.

Notably, cities like Midland and Odessa in Texas, which experienced pandemic-era population declines, were some of the fastest-growing metros in 2024.

7. CO-WORKING SPACES CLIMB 25% IN A YEAR

According to Commercial Edge’s latest National Office Report, co-working locations surged 25% year-over-year through February, coinciding with a 15.2% increase in overall square footage.

Co-working spaces have grown in popularity since the pandemic and are helping to fill a gap in the demand for space by working professionals.

As a percent of total office stock, co-working spaces increased 30 basis points from February 2024 to 2.0% as of the latest tally.

While still a significantly small portion of national office space, co-working’s momentum in individual regions and sectors makes it increasingly important in several local office markets.

The Southeast region of the United States leads in total co-working spaces with 1,960 spaces, up 24.2% year-over-year. The West follows closely with 1,709 spaces and has grown 16.7% in the past year.

In the Northeast, there are a total of 1,422 spaces, which is a 17.5% increase over last February. The Midwest has 1,121 spaces, up 27.7% year-over-year. The Southwest has 999 spaces, up 18.8% year-over-year.

The average size of co-working locations has decreased in the past year, which is expected to continue but mostly reflects the sub-sector’s shift into the suburbs as central business districts gradually normalize.

8. HOMEBUILDER CONFIDENCE

Builder confidence dropped to its lowest level in seven months in March, according to the latest reading from the NAHB/Wells Fargo Housing Market Index.

Both sales conditions and prospective buyer traffic for newly built single-family homes worsened during the month. Sales expectations for the next six months held steady.

According to an NAHB statement following the data release, builders continue to face labor and lot shortages, while tariff issues exacerbate material cost challenges.

Meanwhile, builders are beginning to see regulatory relief, such as in the Administration’s recent pause in the 2021 IECC building code requirement.

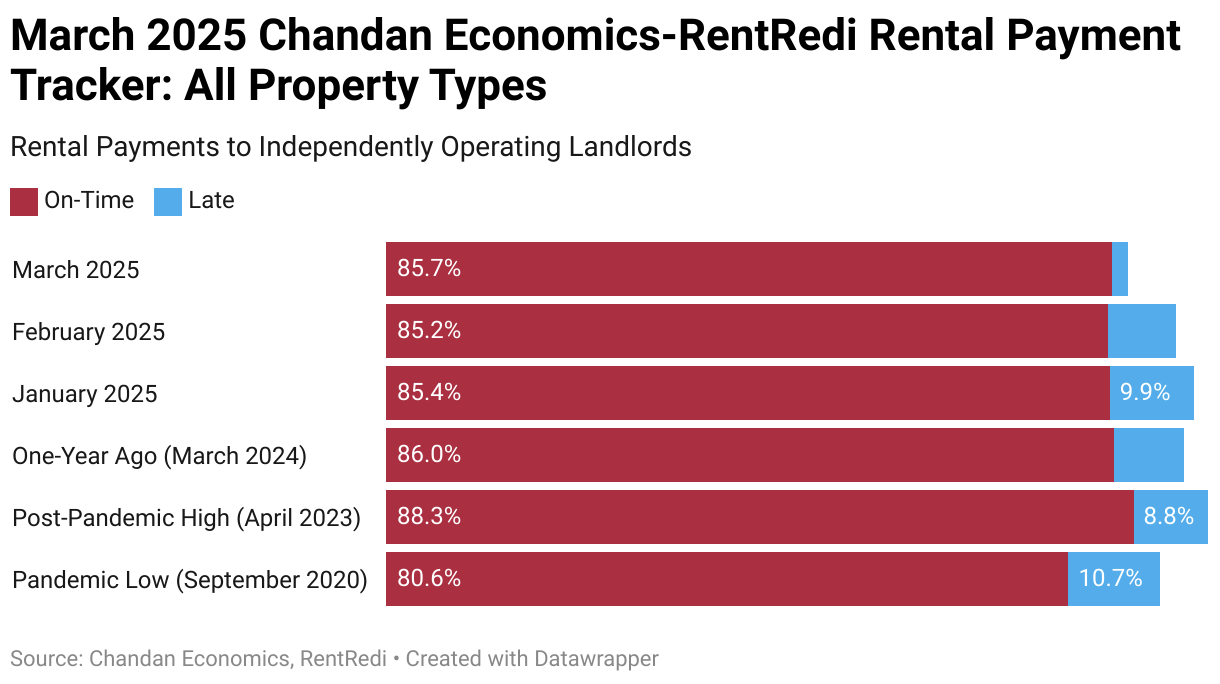

9. INDEPENDENT LANDLORD RENTAL PERFORMANCE

According to the latest Chandan Economics-Rent Redi Independent Landlord Rental Performance Report, in March 2025, the on-time payment rate in independently operated rental units jumped by 53 basis points (bps), rising to 85.7%.

This month’s 53 bps jump was the most substantial single period of improvement in on-time rental payments in two years.

Compared to a year earlier, on-time payments are down slightly by a quarter of a percentage point (-25 bps). On-time collection rates have now fallen annually for the past twenty (20) consecutive months. However, the pace of annual increase has meaningfully lessened in recent months

The forecast full-payment rate improved for the second straight month, rising to 94.7%.

Western states continue to hold the highest on-time payment rates in the country, led by Idaho, New Mexico, Alaska, California, and Utah.

2-4-family rental properties and single-family rentals held the highest on-time payment rates in February, coming in at 85.7%.

10. RETAIL SALES

US Retail sales rose 0.2% month-over-month in February, rebounding from a downwardly revised 1.2% decline in January but still below forecasts.

Seven of the report’s 13 categories registered a decline during the month. This included food services & drinking places (-1.5%), gasoline stations (-1%), clothing stores (-0.6%), motor vehicle & parts dealers (-0.4%), sporting goods, hobby, musical instrument, & bookstores (-0.4%), miscellaneous store retailers (-0.3%) and electronics & appliance stores (-0.3%).

Meanwhile, increases were seen in sales at non-store retailers (+2.4%), health & personal care stores (+1.7%), food & beverage stores (+0.4%), general merchandise stores (+0.2%) and building materials retailers (+0.2%).

Annually, US retail sales grew 3.1%, following a downwardly revised 3.9% increase in January.