On June 18th, the FOMC held interest rates unchanged at 4.25-4.50%, a widely expected decision leading into the meeting.

According to the committee’s statement following the meeting, officials observed swings in net export activity but viewed expanding economic activity as sufficient to justify continuing to hold rates steady for now.

Officials noted that the unemployment rate remains low by historical standards, labor market conditions remain solid, while inflation remains somewhat elevated.

The Fed continues to adopt a wait-and-see approach to interest rate policy, waiting to assess the potential impact of tariffs on prices and the health of the labor market.

2. FOMC ECONOMIC PROJECTIONS

Despite noting sustained elevated uncertainty in the economic outlook, policymakers, on average, continue to pencil in two additional rate cuts before the end of 2025.

Nonetheless, the average member forecast for interest rate moves in 2026 and 2027 has been reduced to just one 25-basis-point cut each year.

Members revised their forecast for 2025 Real GDP growth to 1.4% compared to 1.7% in March. The projection for 2026 was revised down from 1.8% to 1.6%. The outlook for 2025 growth was unchanged at 1.8%.

The unemployment rate is now expected to finish at 4.5% in both 2025 and 2026, slightly higher than in the March release.

PCE inflation is expected to finish at 3.0% by the end of the year, compared to a forecast of 2.7% in March, before reaching 2.1% by the end of 2027.

3. NATIONAL RENT PERFORMANCE

According to the Chandan Economics-Rent Redi, June 2025 Rent Collections report, on-time rental payments in independently operated units dropped meaningfully from May, declining 85 basis points (bps) to 84.3%.

May’s on-time payment rate was revised down to 85.2% from an initially reported 85.5%. In total, the on-time rate has declined by 154 bps over the past three months and has declined year-over-year for 23 consecutive months.

Western states continue to hold the highest on-time payment rates in the country, led by Montana, Utah, Hawaii, Alaska, and Idaho.

2-4-family rental properties rentals held the highest on-time payment rates in June, coming in at 84.6%

Altogether, national rent collection trends indicate that more US renters are struggling to meet their monthly financial obligations, with late payments accelerating more rapidly among younger and lower-income renters.

4. FORECLOSURES FALL

According to ATTOM’s May Foreclosure Report, housing foreclosures decreased by 1.0% in May but remained 9.0% higher over the past year.

The report noted a mixed picture, where fewer foreclosure starts occurred alongside a continued rise in completed ones.

Delaware, Florida, and Illinois posted the highest foreclosure rates in May. Among the top 100 metros, three Florida markets —Lakeland, Cape Coral, and Jacksonville —registered the highest number of foreclosures.

Meanwhile, foreclosure starts increased the most in Texas, Florida, and California, respectively. Nationwide, one in every 4,009 housing units had a foreclosure filing in May.

5. MARKETS MOST EXPOSED TO FEDERAL JOB CUTS

According to a recent analysis by Chandan Economic, while residential and office demand in Washington D.C. stands to be most affected by federal government job cuts, smaller metros with less diverse economies, such as Anchorage, Honolulu, and Charleston (SC), may also be strongly impacted.

Housing inventory in the D.C. area has already climbed substantially during the first half of 2025, up 44.8% year-over-year compared to a nationwide average of 32.5%, according to Altos.

However, compared to relatively smaller and more isolated metros, such as Anchorage and Honolulu, D.C. has a more diversified industry base and is positioned along the nation’s Northeast Corridor—a key engine of economic activity.

While pro-growth elements of the Budget Reconciliation package, which is poised to enact steep federal budget cuts, may spur private investment in these regions, such investments could take time to materialize.

6. POTENTIAL SECTORS FOR OFFICE DISTRESS BUYS

A recent analysis by Trepp suggests that the persistent challenges of the US office sector are slowly opening new opportunities for distressed buys.

Utilizing a nationwide search of office assets with outstanding CMBS loans property and occupancy rates at or below 60%, the analysis identified 279 properties with a total outstanding balance of $9.02 that are potentially strong candidates for distressed buys.

Roughly $3.02 billion of the potential candidates were built before 1940, while another $4.71 billion carry a DSCR of 0.89x or lower, which signals high financial stress for the property.

$6.6 billion of the loans are priced between 3.50% and 5.49%, leaving current borrowers exposed to refi-risks in a higher-rate environment.

Geographically, the New York City metro represented $2.36 billion, or 26%, of the potential properties observed in the survey.

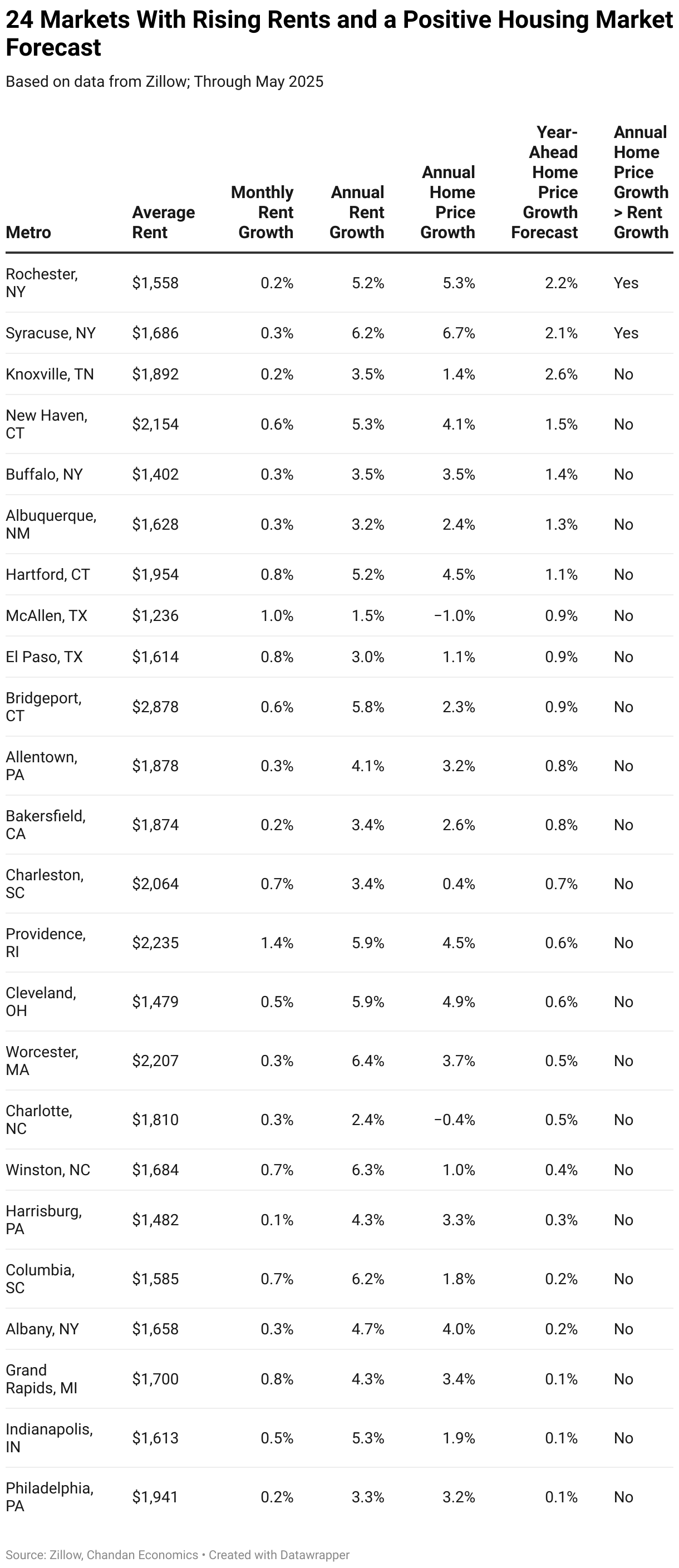

7. MARKETS WITH TOP RENT GROWTH POTENTIAL

According to an analysis by Chandan Economics, among the nation’s top 100 metros, Rochester, NY; Syracuse, NY; and Knoxville, TN, lead markets where rent growth has the most potential to increase over the coming year.

The analysis used a model based on the differential between annual home price growth and rent growth, forecasts for year-ahead home price growth, and recent month-over-month changes to rent prices.

Rochester and Syracuse’s rankings were driven by relative affordability, tight housing supply, and steady population retention. Home prices continue to rise faster than rents in the Empire State metros, signaling that there is room for growth in their rental sectors in the coming year.

Metros like Knoxville, Providence (RI), and Philadelphia rank high due to rising rents and an optimistic home price forecast. Knoxville ranks highest among surveyed metropolitan areas in projected home price increases, according to Zillow’s housing market forecast.

8. BUILDER CONFIDENCE

Builder confidence fell slightly in June, according to the latest Housing Market Index by the NAHB and Wells Fargo.

The survey, which focuses on the pulse of construction activity in the single-family housing market, showed that current sales conditions fell from May, while sales expectations for the next six months also declined. The traffic of prospective buyers also fell slightly.

Perhaps most notably, 37% of builders reported cutting prices in June, the highest percentage since the survey began tracking the share monthly in 2022. The average price reduction for these properties was 5% in June, a figure that has remained roughly consistent since the end of 2024.

9. CONSUMER CONFIDENCE

According to the Conference Board, consumer confidence dropped in June, reversing a sharp uptick in May, with both current and medium-term expectations falling.

Consumers were less optimistic about current business conditions. The average assessment of job availability weakened during the month but remained in growth territory, potentially an early signal ahead of the upcoming Job Openings and Labor Turnover Survey (JOLTS) in July.

The expectation index, which measures consumers’ outlook for future income, business, and labor market conditions, declined to an index level of 69.0, well below the typical recession indicator of 80.

10. RETAIL SALES

According to the Census Bureau, US retail sales declined 0.9% month-over-month in May, following a revised 0.1% decline in April. Sales were worse than the market forecast of a 0.7% drop.

The monthly decline was its largest in four months and could represent a pull-back by consumers ahead of expected tariffs or a deterioration in spending ability.

Sales at motor vehicle and parts stores fell steeply, dropping 3.5% from April.

Building material and garden equipment stores experienced the second-largest decline in any sector, falling 2.7%, followed by gas stations, which dropped 2.0%.