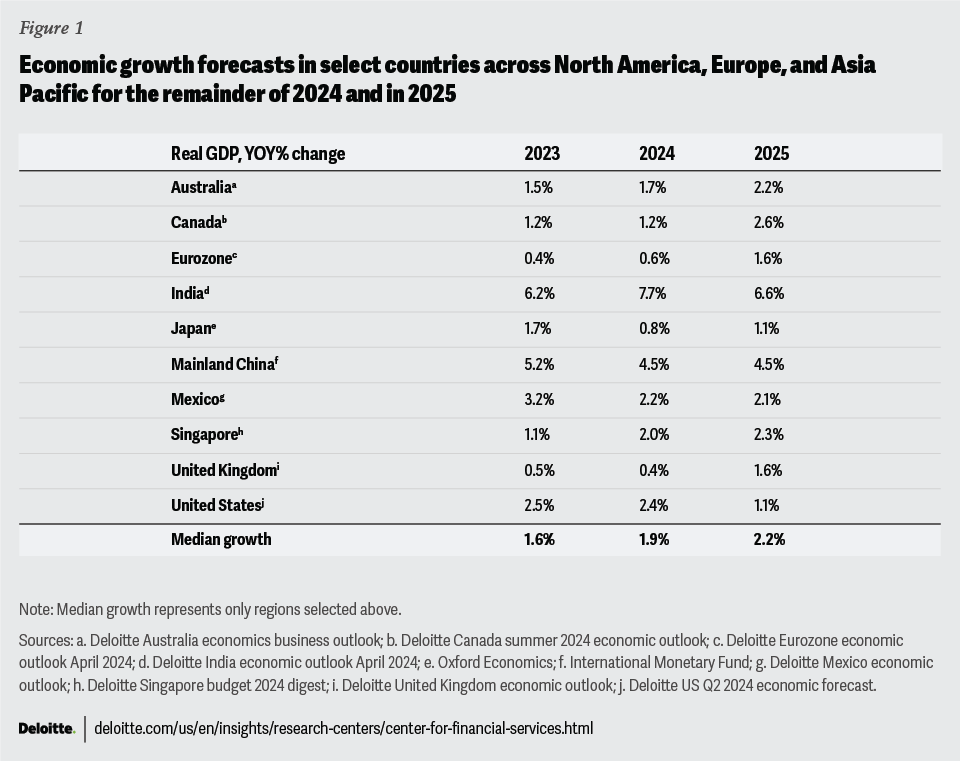

According to Deloitte’s 2025 look-ahead, the current outlook for Commercial Real Estate is dominated by expectations surrounding global interest rates, renewed revenue sentiment, and the potential for industry-wide shifts in areas such as AI, climate resilience, and regulation.

Rates are projected to fall across most major economies in 2025 — however, so is growth. Deloitte’s forecast projects that Real US GDP will fall from a projected 2.4% annual growth rate in 2024 to 1.1% in 2025. The Fed’s interest rate pivot has boosted CRE market sentiment. Still, uncertainty around the timing and volume of rate cuts will keep some capital deployment at bay until things become clearer.

Revenue growth is expected to recover, with 88% of global executives surveyed by Deloitte anticipating higher revenue next year compared to 2024. For context, 60% of executives forecasted declines coming into 2024. In the year ahead, roughly two in three respondents expect revenue to increase by more than 5%.

Data and technology, including AI development, are seen as key drivers of growth in the coming years. 81% of executives plan to increase their technology investments.

Climate resilience also continues to be an increasing focus of CRE leaders. 76% of survey respondents plan to invest in significant energy retrofits over the next 12-18 months.

2. CPI INFLATION

According to the Bureau of Labor Statistics, the Consumer Price Index (CPI) rose 0.2% month over month in October and 2.6% year-over-year, each roughly in line with expectations.

Core-CPI, which removes the more volatile food and energy components, accelerated 0.3% month-over-month, boosted by shelter costs, which accounted for half of the gain in overall CPI. Meanwhile, the energy component held flat while the food index climbed by 0.2% in the month.

Other notable increases included used vehicles, which rose 2.7% month-over-month, and airfares, which jumped 3.2% during the month.

Inflation-adjusted wages increased modestly, rising 0.1% month-over-month and 1.4% from one year ago.

With CPI arriving roughly in line with expectations, the reaction from the interest rate futures market was negligible. At their upcoming December policy meeting, the FOMC is projected to make one additional quarter-percentage-point cut before the end of the year.

3. COMMERCIAL PROPERTY PRICES

According to the MSCI-RCA Commercial Property Price Index, national commercial real estate prices fell just 0.1% month over month and -1.5% year-over-year through October. This performance represents a gradual recovery of commercial prices as the market reaches a cyclical inflection point.

Apartment prices fell by 0.3% from September and 6.1% year-over-year through the end of October. Retail property prices fell 0.1% from September and 1.9% year-over-year.

Industrial again emerged as the only major asset group to post a monthly or annual increase, rising 0.6% month-over-month and an impressive 7.6% over the past 12 months.

The Office sector as a whole fell by 0.1% month-over-month, but suburban office prices climbed by 0.1%. All office segments continue to post year-over-year declines — but suburban office prices have gradually improved this year, resulting in a positive three-month moving average for the broader office sector.

4. INTEREST RATES

According to the Chicago Mercantile Exchange’s Fed Watch Tool, there is a 55.5% chance that the FOMC will follow through with a 25-basis point cut at their December policy meeting, reflecting a relatively split futures market. The forecast has declined from just a week earlier when futures markets priced in an 82.5% probability of cut.

The split sentiment reflects monetary doves who, on the one hand, reference a recent labor market slowdown and shift in the Fed’s dual mandate focus to predict further accommodation. On the other hand, monetary hawks note strong economic growth and Fed officials’ relative caution over cutting too fast as evidence that rates may remain where they are as we turn to the new year.

At the FOMC’s November meeting, the committee voted to cut the Federal funds rate by 25 basis points, following up on their 50-basis point cut in September that began their pivot to accommodative monetary policy.

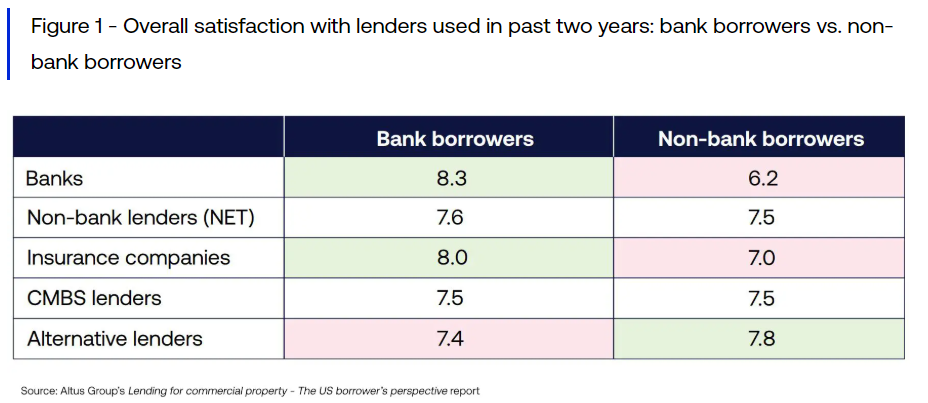

5. NON-BANK CRE BORROWING

A recent Altus group survey investigated the experiences that commercial real estate borrowers have had with non-bank lenders and polled their expectations, recommendations, and challenges.

Borrowers polled expressed a desire for greater efficiency and consistency from their lenders. Bank borrowers expressed higher overall satisfaction with their CRE lenders, while non-bank borrowers referenced flexibility and service as the top factors for their choice.

Non-bank borrowers reported fewer steps to secure financing than bank borrowers. However, their deals tended to move more slowly. Moreover, some expressed higher levels of concern about managing market risks and challenges they expect to face in the coming years.

6. NAHB HOUSING MARKET INDEX

The latest data from the National Association of Home Builders’ Housing Market Index shows that it reached its highest level in seven months during November, exceeding expectations.

The index received a post-election bump, as builders expressed confidence that the Republican sweep of Congress and the White House will increase the likelihood of significant regulatory relief and boost construction activity.

The current sales conditions indicator rose on the month, as did the gauge that measures sales expectations for the next six months. Prospective buyer traffic also posted a modest gain from October.

There was also a modest decline in the share of builders cutting prices and their amounts. 31% of homebuilders slashed prices in November, compared to 32% in October, while the average price reduction was 5%, slightly below the 6% rate posted in October.

7. INDEPENDENT LANDLORD RENTAL PERFORMANCE

According to the latest report from Chandan Economics, the on-time payment rate in independently operated rental units remained flat at 85.5% in November compared to the previous month.

On-time collections are down by 70 bps from a year earlier. Moreover, compared to the post-pandemic peak of 88.2% set in April 2023, on-time payments are down by 279 bps, reflecting some sustained performance deterioration.

Still, there are signs that on-time collections are stabilizing. For the past five months of data, on-time payment rates have held between a low of 85.3% and a high of 85.7%.

Trends within key rental subsectors reveal a slight performance gradient. Of the three tracked property sub-types, properties with 2-4 rental units and single-family rentals (SFR) led the way in November 2024, with the two subsectors holding an on-time payment rate of 85.7%, respectively. Multifamily properties sat slightly lower at 85.1%.

Measured by State, western-located properties continue to outperform the rest of the country. In November 2024, on-time payment rates stood highest in Alaska (93.7%), followed by Nevada (91.9%), Utah (91.4%), Colorado (91.4%), and New Mexico (91.1%).

8. ENGINEERING & CONSTRUCTION INDUSTRY OUTLOOK

According to Deloitte’s 2025 Engineering and Construction Industry Outlook, the improving interest rate outlook, technological integration, and navigating the policy landscape will guide the industry over the next year.

Falling rates are expected to boost construction demand across various segments and create growth opportunities in 2025. However, labor market challenges persist. The engineering and construction sector faces a significant talent shortage, posting an average of 382k job openings between August 2023 and July 2024.

Cost overruns from inflation and interest rates will incentivize firms to focus on value creation and sustaining growth through strategic divestitures and rebalancing capital allocation. Large construction firms may optimize portfolios by divesting noncore assets and doubling down on core investments.

Like other sectors, adopting AI and other digital tools to enhance productivity and address labor gaps will be crucial to the engineering and construction field. Technologies such as digital twins, robotics, and generative AI will continue to transform operations in the industry.

The policy outlook is also key. Recent federal investments through the Infrastructure Investment and Jobs Act (IIJA), the Inflation Reduction Act (IRA), and the CHIPS and Science Act will continue to trickle into markets in the coming year. The activity is expected to drive growth in the manufacturing and energy sectors and generate downstream demand for engineering and construction firms.

9. HOUSING INVENTORY REBOUND

According to a recent analysis by ResiClub, 54 of the nation’s 200 largest housing markets have inventory levels above their pre-pandemic levels, a significant jump from just 17 at the end of 2023.

From October 2019 to October 2021, the number of US actively listed homes fell from 1.2 million to just 566k, a 53% drop in just two years.

However, inventory is gradually recovering, reaching 954k through October 2024, still a large but more modest 21% below the 2019 benchmark.

Smaller markets have tended to be the ones to see the most recovery. Huntsville, AL, Killeen-Temple, TX, and Lubbock, TX, have experienced the strongest post-pandemic recoveries but rank 108, 119, and 162, respectively, in national metro size.

The Bridgefield-Stamford-Norwalk, CT metro remains the furthest below pre-pandemic levels, followed by Connecticut’s largest metro area, Hartford-East Hartford-Middletown. Peoria, IL, ranks the third furthest below 2019 levels.

10. NMHC QUARTERLY SURVEY OF APARTMENT CONDITIONS

According to the Q3 NMHC Survey of Apartment Conditions, Multifamily financing and sales volume reached their highest level since 2022 during the third quarter.

43% of respondents reported higher sales in Q3 2024 compared to 32% during the previous quarter. With the Fed’s first interest rate cut only coming in September, the early pace of thawing deal activity is an encouraging indicator for the sector.

The equity financing gauge rose from an index level of 49 in the previous quarter to 67 in the Q3 reading. In October 2023, the reading stood at just 18.Optimism increased around debt financing, with 62% of respondents seeing now as a better time to take out a Multifamily mortgage, compared to just 37% who expressed this sentiment in Q2.

Looking market to market, 38% of respondents listed “primary markets” like New York, San Francisco, Los Angeles, and Miami as benefiting from sales activity better than the secondary or tertiary markets that dominated initial post-pandemic activity. Still, roughly 45% saw no change.